Practice area · 04/08

Model validation.

Credit, market, AML, and AI/ML models — independently validated, conformant with SR 11-7, and written for examiners to read.

Credit, market, AML, and AI/ML models — independently validated, conformant with SR 11-7, and written for examiners to read.

A validation report should hold up to an examiner — and to the modeler whose model it covers.

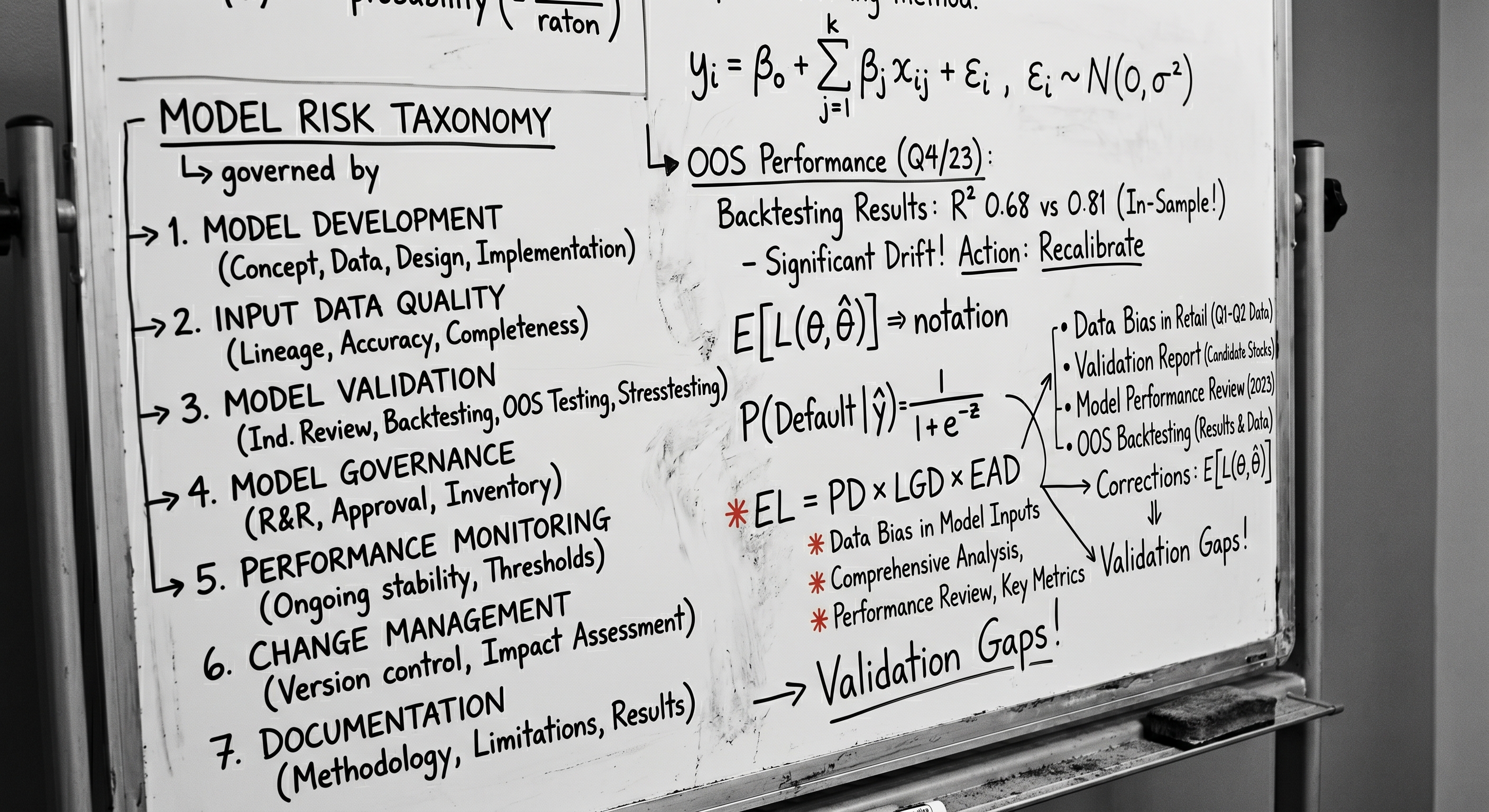

The SR 11-7 framework asks for independent validation across three dimensions: conceptual soundness, ongoing monitoring, and outcomes analysis. Done well, a validation gives the model risk committee real comfort. Done poorly, it gives them a 60-page document that says 'no material issues identified' and an examiner who finds three.

Our practice covers credit risk models (PD/LGD/EAD, CECL, CCAR loss forecasting), market risk models (VaR, sensitivity, stress), AML transaction monitoring models (rule sets and machine-learning hybrids), and the increasing class of AI/ML models used in underwriting, fraud detection, and customer-facing applications. For each, we validate against the data, the assumptions, the implementation, and the use.

The validator has to understand the model. That sounds obvious; it is what most validation reports fail at. Edgar built his career as a quantitative practitioner before he became a validator. The reports our practice produces show the math; they do not paper over it.

PD/LGD/EAD, CECL allowance models, CCAR/DFAST loss forecasting, scorecard models.

VaR, expected shortfall, sensitivity, scenario and reverse-stress models.

Rule-set calibration, threshold tuning, hybrid ML-based detection systems.

Underwriting, fraud, churn, and customer-facing models — including fairness, explainability, and drift monitoring.

Theory, assumptions, choice of methodology, alternatives considered, data appropriateness.

Backtesting, benchmarking, sensitivity, monitoring plan, threshold setting.

Model documentation reviewed, data dictionary received, scope confirmed with model risk management.

Independent replication on the same data; alternative specifications considered.

Sensitivity, stability, fairness (where applicable), backtesting, benchmarking.

Findings rated, validation report drafted, MRMC presentation prepared.

Quantitative Risk · Analytics · MIT

Edgar holds a Ph.D. in Operations Research from MIT and has spent twenty-five years in quantitative risk and analytics — co-leading Mercantil's Global Risk Management and serving as CDAO at iuvity. He validates models the way he would want his own validated.

We do not build or operate models that we also validate. Independence here is not a preference — it is the regulatory baseline. If we have built a model for an institution, we will not be the firm that validates it.